By now, we are all familiar with the axiom that 90% of startups fail, often within the first year. With the odds seemingly stacked so heavily against success, some may wonder why anyone would want to try and start a startup at all. What these naysayers fail to acknowledge, however, is the enterprising spirit that compels entrepreneurs to pursue their dreams and their vision, despite the risks involved. By nature, entrepreneurs are dreamers. They think beyond the “now.” They’re problem-solvers, disruptors, innovators. And yes, they are also risk-takers – as they need to be, as we all know that only one in ten will succeed.

Even so, nobody wants to fail when they set out to start a startup. What, then, can budding entrepreneurs learn from the failure patterns of the 90% club – and how can they avoid joining it?

What Makes a Successful Startup?

While the oft-quoted 90% figure is familiar enough, there is very little research into the factors that drive the startup failures it represents. The good folks at CB Insights recently decided to dig into the data on startup death to come up with insights into the issue. The effort revealed that 70% of tech startups usually fold 20 months after their first funding, represented by an average of $1.3 million. Consumer hardware companies, meanwhile, had a much higher mortality rate – 97%.

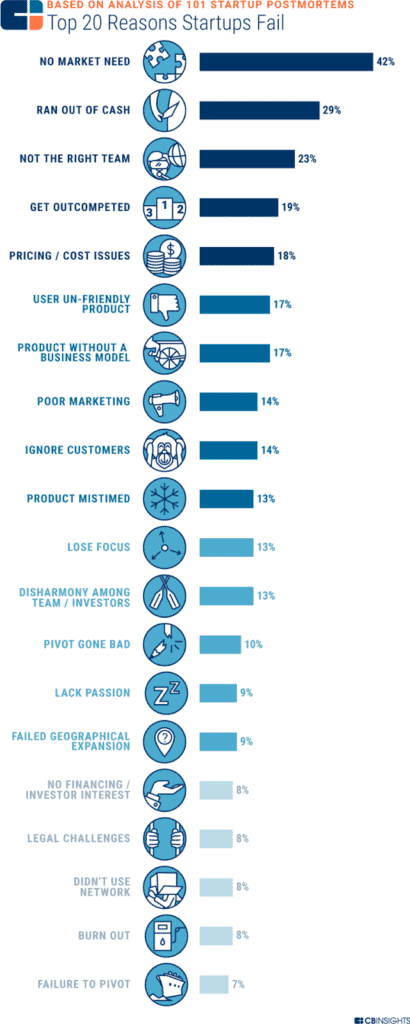

Furthermore, CB Insights analyzed 101 startup failure postmortems to identify the top 20 reasons for the failure of startups. Of course, there is likely to be a combination of reasons that contribute to a downfall of a given startup. Interestingly, however, almost every one of the reasons for failure on CB Insights’ list – like the importance of product-market fit, or productive team dynamics – almost invariably figures in most lists about the attributes of successful startups. In other words, if you’re planning to start a startup, your ultimate success or failure would seem to pivot on the particular successes or failures of a number of key factors.

(Image source: cbinsights.com)

Let’s explore, then, the top five reasons for the failure of the majority of startups – and thereby what you should aim to avoid when you start a startup of your own.

Most Common Pitfalls to Avoid when You Start a Startup

- Solving Problems that Don’t Have a Market

The importance of the “idea headlines almost every article about successful startups.” Starting a startup with an idea is sound advice that is simultaneously pertinent for almost any field of human endeavor – yet one of the most difficult to execute. For instance, is it even possible to sit down and think of an idea for a startup? Well, you could follow Box CEO’s suggestion and pick “the stodgiest, oldest, slowest moving industry you can find” and figure out how to reinvent it. However, merely compelling oneself to sit down and think of startup ideas could more often lead to “made-up” or “sitcom” startup ideas rather than innovations.

Every successful startup is, first and foremost, a problem-solving company – the central idea has been to address a problem that has thus far been underestimated, ignored, or underserved. The sharing economy was built on ideas that address problems in traditional marketplaces, like accommodation or transport, by leveraging P2P assets and services. In a technocentric society, it’s easy to be tempted to start with technology rather than a problem – an approach that will, in all probability, struggle to find a market. And yet, the CB Insights analysis reveals that ideas that address problems without an underlying market need are the number one reason for startup failure, accounting for up to 42% of all studies cases.

(Image source: ideou.com)

Even the most empirically promising ideas do not necessarily translate into technologically or commercially addressable opportunities. This is where human-centered approaches, such as design thinking can help validate startup ideas against three critical criteria:

- The idea is desirable from a human point of view.

- It is feasible given the tools and technologies of the day.

- It is economically viable in that it is commercially credible, scalable, and sustainable.

Resolving the tension between these variables is the first step towards creating a profitable and sustainable startup idea. Startups can even use design thinking’s simple, five-step, iterative process – empathize, define, ideate, prototype, and test – to address complex and often loosely-defined problems without losing sight of the central promise of the idea.

Many startups are also turning to a business model canvas – a one-page template that captures the startup business model on a single sheet of paper – as an alternative to traditional multiple page business plans.

(Image source: wikipedia.org)

This template provides a holistic view of the business and evolves to reflect new information and new assumptions that need to be validated, as the Netflix business model canvass exemplifies.

(Image source: innovationtactics.com)

- Running Out of Cash

Cash flow issues are the second most common contributor to startup failure after product-market fit. In fact, a cash flow drought could even be the terminal symptom of many other causes for startup failure, including the absence of market need, bad team dynamics, etc.

The concept of capital runway refers to the period of time, typically months, that a startup can survive before the next round of capital infusion or bankruptcy – whichever comes first. Though the runway can vary across different industries, business models, and growth stages, the general recommendation for capital runway among startups is 12 months.

(Image source: nordea.com)

However, understanding and managing a company’s cash runway is not just about crisis planning; it’s about building a financially successful business that is capable of anticipating and calibrating expectations around how cash flow, profitability, and funding needs intersect. This is why scenario planning and financial modeling are important for everyone who wants to start a startup, no matter the funding or growth stage of the business.

There are two different approaches that startups can take when it comes to financial modeling – top-down and bottom-up.

(Image source: matter.health)

The top-down approach starts with an understanding of the macroeconomy, industry estimates, and the dynamics of the target market to arrive at realistic forecasts of revenue and growth that fit a specific startup’s operating profile. With the bottom-up approach, the focus is less on external factors and more squarely on key internal company capabilities, attributes, and value drivers.

Both approaches have their advantages and their drawbacks. For instance, the bottom-up approach is always going to be more realistic as it works projects outwards based on a startup’s unique combination of resources and limitations. In contrast, the top-down model could possibly engender a degree of forecasting optimism that is based more on the size of potential rather than a firm’s ability to capitalize on it. The best strategy would be to combine both models, either by starting with top-down and gradually transitioning to bottom-up as internal metrics and data become more readily available, or by using the former for long-term forecasts and the latter for short-term targets.

- Lacking the Right Team

It’s not rare for the founding members of a startup to be reconstituted as the business scales. In fact, 20% to 40% of founders are substituted for professional managers at critical transition points during a startup’s growth. More often than not, these replacements are driven by the long-term growth interests of the business rather than the competencies of the founders.

However, some of the stories that emerge from the CB Insights postmortem – like the wish to have a CTO or a founding team that could build an MVP – highlight why team composition ranks so high as a cause of startup failure.

There is no underestimating the challenge of attracting the right mix of knowledge, experience, and attitude to a startup environment that is typically characterized by risk and uncertainty. Then there is the fact that most startup teams come together of their own volition rather than through a tried and tested process that rigorously vets candidates and maps them to clearly defined roles and responsibilities. And yet, the founding team is perhaps as important as the central idea that they are expected to execute and scale.

Today, there are specialist startup talent accelerators and investors, such as Entrepreneur First and Ianuly, offering recruitment models targeted at the startup community. Entrepreneur First, for instance, invests in individuals “pre-team, pre-idea” to help create technology startups. The company, backed by a host of influential technologists and investors, including the founders of LinkedIn, DeepMind, and PayPal, has thus far created over 300 companies with a combined portfolio value of $2 billion. Ianuly, meanwhile, works with venture-backed startups in aggressive growth mode to provide them with key leaders and complementary teams while they focus on growing the business.

- Getting Outcompeted

It’s called the “competitive landscape” for a reason – no matter how unique or original you think your idea is when you start a startup, sooner or later, you will be facing numerous competitors, all battling your business for customer wallet share. It might be a big company that spots what you’re doing and decides to use its superior firepower to blast you out of business or several smaller companies that emerge to try and kill you off with a thousand little bites. Either way, getting outcompeted was the fourth most common reason for startup failure, cited by 19% of CB Insights’ respondents.

As a spokesperson for children’s apparel delivery box service Mac & Mia (now defunct) told CB Insights: “Mac & Mia faced a host of competitors in the children’s delivery box space, including Stitch Fix, which launched its kids clothing service in 2018. Stitch Fix went public in 2017 and had a market cap of around $2.7 billion. At least 20 other upstarts have launched similar delivery services for children’s clothes.”

You can’t avoid competition when you start a startup – no business exists in a vacuum, and if you think you’re the “first and only” company to do what you do or offer what you offer, think again. The name of the game is instead to avoid being outcompeted by your rivals – and that means conducting competitive analysis.

(Image source: mykopono.com)

A competitive analysis is a process of identifying precisely who your competitors are and evaluating their products, strategies, services, prices, and marketing messages to determine their strengths and weaknesses relative to your own business model. And if you really do think you’re the “first and only,” then perhaps you should build some extra room into your definition of “competitor.” Even if your target customers aren’t using a product or service exactly like yours to solve a problem, they’re probably using some kind of alternative – and the producer and seller of that alternative is a competitor for your business.

Myk Pono, Senior Product Manager, Growth & Acquisition at Barracuda, provides a handy way to think about your competition when you start a startup.

(Image source: mykopono.com)

- Pricing/Cost Issues

Needless to say, when you start a startup, devising a viable product pricing strategy is an essential piece of the puzzle – and notoriously difficult to get right. Pricing is a balancing act – it needs to be low enough to attract customers, yet high enough to eventually cover costs.

Failure to strike this balance was what led to the downfall of scientific wellness startup Arivale. Despite many other successes, in the end, the cost of running the company proved too high compared to the revenues it generated: “Our decision to terminate the program comes despite the fact that customer engagement and satisfaction with the program is high and the clinical health markers of many customers have improved significantly. Our decision to cease operations is attributable to the simple fact that the cost of providing the program exceeds what our customers can pay for it. We believe the costs of collecting the genetic, blood, and microbiome assays that form the foundation of the program will eventually decline to a point where the program can be delivered to consumers cost-effectively. Regrettably, we are unable to continue to operate at a loss until that time arrives.”

(Image source: marketingtutor.net)

Once again, success comes down to doing your homework. You need to know your customer, know your product and know your market – inside and out. You need to know your customer acquisition costs, your marketing costs, material costs, salary costs, rent costs – the total costs to deliver your product or service from the ground up, as it all needs to go into how your product or service gets priced.

You also need to evaluate the competition – but you must be careful. Although you can figure out roughly your customers’ willingness to pay (WTP) by taking a look at the pricing strategies of your competitors (if they’re willing to pay $50 for your competitor’s offering, they should be willing to pay the same for yours), you must remember that your product or service should be inherently different – and should, therefore, be priced differently.

Speaking of the competition, you will need to keep a close eye on any new players that enter your space. When you start a startup, though you will unlikely be a true “one and only,” the market may not be too crowded – so you can justify keeping your prices high. However, over time, you should expect new low-cost entrants to emerge. If you’re not careful, these players will steal your customers one by one until it’s too late to react, and you’re left wondering where it all went wrong.

You must also be careful if you want to start a startup that goes after an incumbent. A price war will soon emerge, and though you may have lower costs, established players have deeper pockets – and you will lose.

Final Thoughts

Of course, these are just the top five reasons, out of a total of 20, for startup failure that came out of CB Insights’ postmortem analysis of over 100 shuttered business. And, as mentioned earlier, almost each one of these reasons also figures quite regularly on lists of attributes required to start a startup successfully. All of which just goes to show that knowing what works (and what doesn’t) when you start a startup is the easy part – executing it and marking it work is the real challenge. Good luck!

Summary:

Why startups fail

By now, we are all familiar with the axiom that 90% of startups fail, often within the first year. It is the enterprising spirit that compels entrepreneurs to pursue their dreams and their vision, despite the risks involved. Let’s explore, then, the top five reasons for the failure of the majority of startups – and thereby what you should aim to avoid when you start a startup of your own. Most Common Pitfalls to Avoid when You Start a Startup: 1. Solving Problems that Don’t Have a Market 2. Running Out of Cash 3. Lacking the Right Team 4. Getting Outcompeted 5.Pricing/Cost Issues. Success comes down to doing your homework. You need to know your customer, know your product and know your market – inside and out. You need to know your customer acquisition costs, your marketing costs, material costs, salary costs, rent costs – the total costs to deliver your product or service from the ground up, as it all needs to go into how your product or service gets priced.